So far, the agentic payments experience hasn't happened.

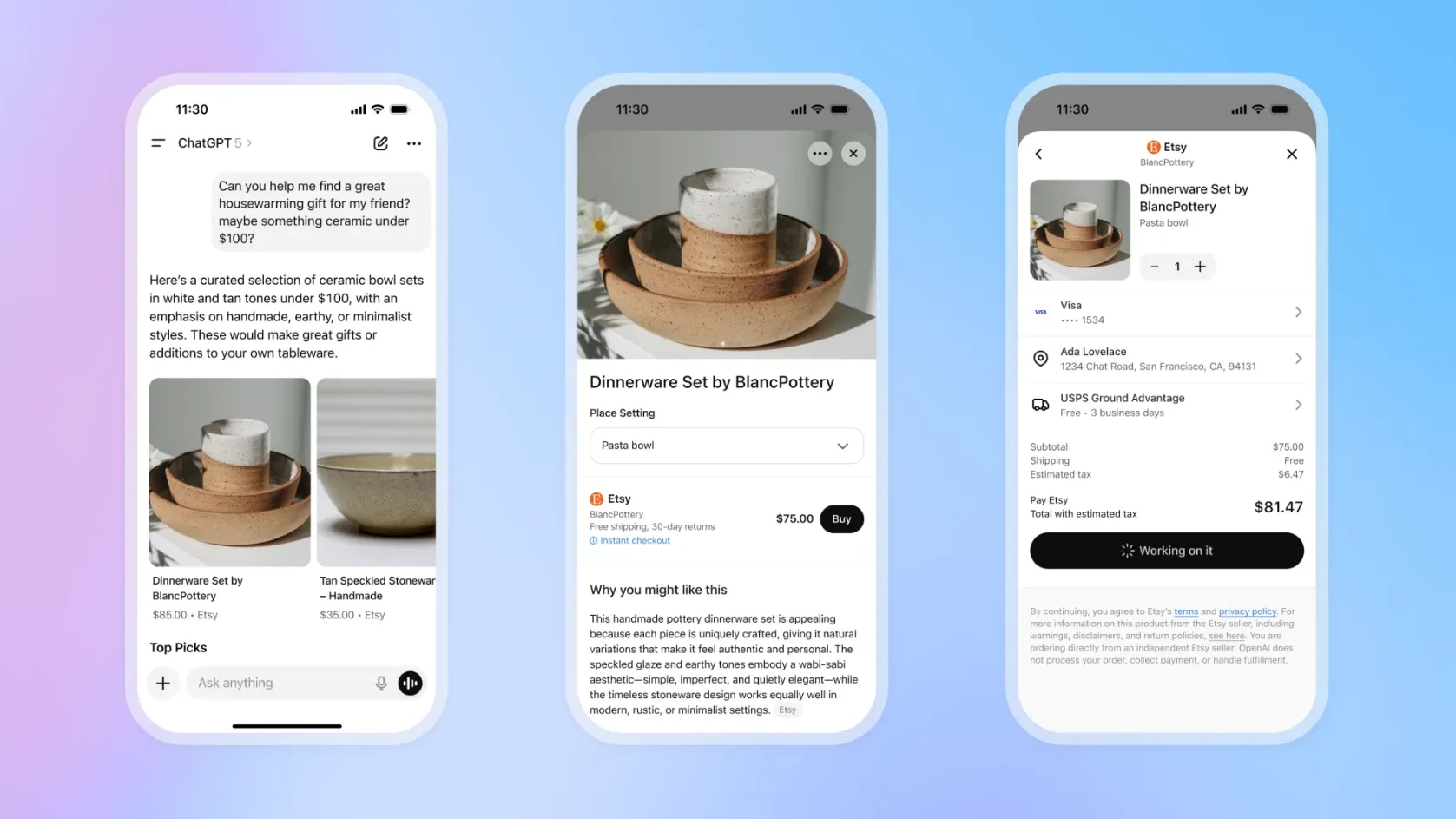

In September 2025, OpenAI launched Instant Checkout in ChatGPT, powered by Stripe. By January 2026, reporting confirmed a 4% fee on completed transactions, favorably less than Amazon's 8–15%. For the industry at large, this seemed to be the symptom of the brave agentic world finally happening: consumers would complete a check out without leaving the LLM.

But then, by March 2026, the model was shut down. The fee was dropped, native in-chat checkout was deprioritized, and an OpenAI spokesperson confirmed the pivot: “We are evolving our commerce strategy within ChatGPT to better meet merchants and users where they are. Instant checkout is transitioning to apps, where purchases can occur more seamlessly.”

With OpenAI and Stripe having been hailed as the first to lay standardized rails for AI-agent commerce, this reversal left executives uncertain about whether true agentic commerce is happening at all.

Of course, the answer to what went wrong is not that AI failed. But rather that payments, as OpenAI learned, are harder than they look from the outside - and agents, by design, are not payments experts, nor should they be.

Where agentic has worked and where it still hasn’t

The clearest successes in agentic have so far come from B2B. For example, in late 2025, Ramp launched AI agents for procurement and accounts payable, automating invoice coding, approvals, and payment execution. Unlike most payment innovations, which typically debut in B2C, agentic technology has advanced faster in B2B: consumer commerce simply lacks the same guardrails. Agents in a corporate environment operate within defined policies against approved counterparties.

However, the audience for consumer agentic commerce is undeniably there. By early 2026, ChatGPT reached 900 million weekly active users and Forrester data shows 33% of US online adults had used AI agents to find and compare products in the prior three months.

Still, those same stats show that only 10% had used an AI agent to make a purchase, and 61% said they would not be comfortable doing so. Even among those familiar with OpenAI’s Instant Checkout, only 8% had used it to buy something.

This data signals that the payment layer that can convert search into a transaction for the masses does not yet exist.

Why agentic payments are inherently complex

For an AI agent to complete a consumer transaction reliably, it needs four things:

- Live product feeds with accurate pricing and real‑time inventory

- Explicit, verifiable consent at the moment of authorization

- Fraud models designed for agent behavior, not human behavior

- End‑to‑end tax, compliance, and dispute handling across jurisdictions

As of early 2026, no platform today has solved all four simultaneously.

With that said, the example of Instacart offers a useful preview of what works within these constraints. As the first grocery partner to offer an embedded checkout experience inside ChatGPT, it succeeded because it had real-time inventory across 100,000 stores and 1.8 billion product instances, which is something most merchants don’t have. When OpenAI pulled back, Instacart shifted to the embedded fulfilment layer. Today, ChatGPT handles discovery, while Instacart handles checkout and fulfilment.

That division of labor, where merchants own the transaction and LLMs drive discovery, is a model that works today, but it will not be the model in three years, when agents become autonomous.

What happen when liability shifts to agents

When discussing problems of agentic payments, most industry players assume that the biggest problem with agentic is liability: “When a consumer delegates a purchase to an AI agent and something goes wrong, who is responsible?”

Both Visa and Mastercard are resolving the liability question by developing agentic payment pilots using existing rails. To this day, neither has launched a scaled, autonomous agent payment product. The market is still in the PoC and early‑partner phase.

But what’s more interesting is that as true delegation occurs, liability will shift to the agents themselves. Suddenly, the agent that initiates the transaction becomes the accountable party. When this happens, it will represent a fundamental restructuring of how commerce is authorized, verified, and settled, one that touches every layer of the payments stack.

For payments infrastructure providers like Nuvei, this duality is the defining challenge. Serving merchants under the current Merchant of Record model is one problem but serving agents as they become transacting principals is another. To this day, few providers are positioned to do both, and it’s a space where Nuvei is currently building.

The protocol race and how Nuvei is becoming the universal translator

Launched at NRF in January 2026 and co-developed with Visa, Mastercard, Nuvei, and 20-plus others, Google’s Universal Commerce Protocol (UCP) covers the full commerce lifecycle — discovery, cart, checkout, and post-purchase, while keeping the retailer as Merchant of Record. On the other side of the world, Alipay and Alibaba’s Agentic Commerce Trust Protocol serve the same function but within the super-app ecosystem.

To this day, no protocol has locked in dominance, which explains why merchants like Shopify co-develop both Google's UCP and OpenAI's ACP as a hedge. The race is genuinely open. What is not open is the underlying requirement: any agent, operating on any protocol, still needs to move money and that means connecting to payment rails that most protocols were not designed to navigate.

That is the problem Nuvei is buidling to solve with Protocol Compatibility Layer (PCL). Rather than betting on a single standard, the PCL connects to any protocol through a single call, translating across payment rails regardless of which agent or commerce framework sits above it. In a market where protocol dominance is unresolved and merchant hedging is rational, the only durable infrastructure is the one that is agent-agnostic and protocol-agnostic.

Where acquirers add value in agentic commerce

Of course, not every merchant will want fully autonomous agent transactions. Some will want human confirmation above certain thresholds, or restrictions on what agents can modify - delivery address, subscription terms, spending limits. Acquirers are the natural party to build and manage that merchant preference layer, and to enforce it consistently across every agent, protocol, and rail.

Current fraud models are built around human behavioral patterns, but agent-initiated transactions look fundamentally different: higher frequency, more systematic, potentially spanning multiple merchants in rapid succession. Acquirers who retrain their risk models for agent behavior early will have a material edge and a genuine value proposition for merchants nervous about opening their checkout to non-human buyers.

Agents will also generate extraordinarily clean transaction data: structured, consistent, with clear intent signals. Acquirers like Nuvei sitting on that data are well-placed to turn it into actionable intelligence - conversion analysis, agent journey mapping, drop-off by agent type. In this world, the acquirer's role shifts from passive processor to active infrastructure partner: one that uses data to tell a story about customers that was simply impossible before agentic commerce existed.

Fundamentally, the right payments partner brings something each participant in the agentic ecosystem cannot provide for itself. For agents, that means a trusted execution environment, a payments layer that handles authorization, compliance, and settlement without the agent needing to understand any of it. For merchants, it means global governance and trust delivered through multi-method design: the right payment method, in the right market, under the right regulatory framework, regardless of which agent initiated the transaction. And for platforms and distributors, it means the fastest path to agentic readiness without rebuilding infrastructure from scratch.

The missing step: choosing the right payments partner

What often gets overlooked is that none of this should be built by merchants alone. Positioning for agentic commerce does not mean becoming an expert in agent trust, network mandates, or cross‑protocol authorization. It means working with a payments partner that can act as a trusted intermediary for both merchants and agents.

The right partner allows merchants to focus on what they do best: catalogue readiness, pricing strategy, fulfilment, and customer service. While the payments layer absorbs the hard parts: accepting only trusted agents, enforcing merchant‑defined consent and spending rules, and connecting seamlessly to card networks, alternative payment methods, and emerging agent protocols. In practice, this means filtering agent traffic before it reaches checkout, validating cryptographic mandates as they emerge, and routing transactions through the appropriate rails without requiring merchants to rebuild their stack every time a new framework appears.

As agentic commerce scales, merchants that try to solve this alone will either over‑restrict access (limiting upside) or over‑expose themselves to risk. Those that work with a payments partner designed to serve both sides of the transaction will be able to move faster, open their checkout safely to non‑human buyers, and stay adaptable while the protocol landscape is still in flux.

We haven’t failed in agentic commerce - we're still building the foundation.

OpenAI and Stripe moved faster than the infrastructure beneath them was ready for.

In 2008, the iPhone had already proven that people would buy through a phone. What didn't exist yet were the app stores, mobile payment rails, and touch-optimized checkout flows that made mobile commerce a category worth building a business around. The infrastructure followed the intent, not the other way around. Agentic commerce is at the same inflection point: the intent is established, but the infrastructure around it is still being built.

What happens at checkout is a different discipline entirely, one that requires navigating local payment methods, acquiring relationships, fraud signals, and cross-border complexity that no general-purpose agent was built to handle alone. This is why selecting the right payments partner to absorb that complexity is a strategic decision – one that merchants need to make, whether the consumer came from the agentic flow or not.

What will define the category in the future are the protocols that earn trust, the liability frameworks that achieve legal clarity, and the payment layers that can route any transaction initiated by any agent on any rail. And that is exactly where Nuvei is building with its Protocol Compatibility Layer (PCL): not for a single protocol, one agent framework, or one definition of what agentic commerce becomes - but to ensure global merchants are able to capture the maximum upside when the standards settle, whichever ones do.

Because when agentic commerce finally clicks, the winners won’t be the agents that talk best, but the payment layers that can execute flawlessly, no matter who’s speaking.