La caja es la marca: en qué confían realmente los consumidores estadounidenses

Los nuevos datos de Nuvei sobre los consumidores muestran que el pago es un acto deliberado y que los métodos de pago que ven los consumidores al finalizar la compra inspiran más confianza que la marca que los rodea.

Los comerciantes de todo el mundo invierten mucho en su marca: en la creatividad, el posicionamiento y la experiencia que lleva hasta el momento de pagar. Pero en el momento en que un consumidor decide si va a gastar su dinero, lo que importa es que la infraestructura que hay detrás del botón de compra se ajuste a la forma en que espera pagar.

Según la reciente encuesta «How America Pays» de Nuvei, realizada a 1.000 consumidores estadounidenses (abril de 2026), casi uno de cada tres consumidores estadounidenses (37 %) preferirá abandonar una compra antes que completarla con un método de pago que no haya elegido. No porque el producto o la experiencia les hayan decepcionado, sino porque, al no disponer de los métodos de pago adecuados que los consumidores conocen y en los que confían, el proceso de pago les ha fallado.

Un proceso de pago fallido no solo supone perder una venta. Supone perder la relación.

La evolución de la confianza en el comercio mundial

Desde sus inicios, el comercio siempre ha requerido confianza. Cuando los pagos eran físicos, la confianza era visible: el dinero en efectivo cambiaba de manos, los productos cambiaban de manos y ambas partes podían verlo en tiempo real. Cuando las tarjetas sustituyeron al dinero en efectivo, esa garantía visible desapareció, y el sector la reconstruyó mediante firmas, chips y PIN, y las capas de autenticación que ahora sustentan las transacciones digitales.

Cada cambio sucesivo exigía a los consumidores que depositaran su confianza en sistemas que no podían ver del todo, y cada cambio tenía que ganarse esa confianza. Lo mismo ocurre ahora, solo que aún más, sobre todo con el auge de la automatización. A medida que el comercio se ha trasladado a Internet y el proceso de pago se ha convertido en el principal punto de contacto entre empresas los clientes, la confianza se ha concentrado cada vez más en la propia experiencia de pago.

La pregunta hoy es si las empresas llegar al consumidor, sin importar quién sea ni dónde esté, justo en el momento en que está listo para pagar.

Cuando los consumidores ven un método de pago que les resulta familiar, la conversión no se hace esperar. Cuando no es así, la encuesta lo deja claro: muchos se van.

El 61 % de los consumidores estadounidenses elige activamente cómo pagar según lo que más les convenga. Pero para cuando el cliente llega a la caja, esa decisión financiera suele estar ya tomada. La función empresasen ese momento no es convencer, sino confirmar.

Cuando falta un método preferido, más del 30 % de los consumidores se van. El abandono del carrito, una métrica que la mayoría de los comerciantes siguen de cerca, suele ser un problema de cobertura de métodos que se manifiesta como un problema en el embudo de conversión. Esta brecha pasa fácilmente desapercibida en los análisis. Se nota más claramente en la pérdida de ingresos.

Esta tendencia es aún más evidente a nivel internacional. En muchos mercados, los métodos de pago locales no son simples extras opcionales, sino que forman parte de la infraestructura financiera estándar. Su ausencia no supone una simple carencia en el catálogo de productos, sino una barrera estructural para la conversión en ese mercado.

Las formas de pago son ahora un elemento distintivo de la marca

Los pagos son, por definición, algo personal. Cuando un consumidor saca la cartera, está mostrando su identidad financiera: el banco que usa y el que usan sus padres y amigos, la línea de crédito que gestiona, la app en torno a la cual ha construido parte de su vida financiera, dependiendo de dónde viva y a qué grupo demográfico se identifique. Impedir esa elección al pagar da la sensación de que empresas entiende cómo paga realmente el cliente, lo que significa que no entiende al cliente.

Casi uno de cada tres consumidores estadounidenses afirma que las opciones de pago influyen en la percepción que tienen de una marca, no solo en si completan la compra, sino también en lo que opinan de la empresa. Además, un 29 % afirma que la marca del minorista por sí sola no basta para que se sientan seguros al finalizar la compra; necesitan métodos de pago que les resulten familiares para salvar esa brecha de confianza.

Quizás el hallazgo más revelador de esta encuesta fue que el método de pago tiene más peso que la marca: un logotipo de pago que les resulte familiar transmite a los compradores una sensación de seguridad. Cuando no está ahí, la fricción no es solo una molestia. Es una venta perdida. Por el contrario, las empresas poco o ningún reconocimiento de marca pueden generar ingresos gracias a los clientes simplemente por la confianza que estos depositan en los métodos de pago que reconocen.

La oferta de métodos de pago no es una partida de gastos. Es una decisión de marca que repercute en los ingresos.

Para un director de operaciones (CRO) o un responsable de pagos, esto cambia la cuestión de dónde invertir. Las empresas un GMV considerable, incluso con un aumento modesto en la conversión de la cesta de la compra gracias a una mayor variedad de métodos de pago, tienen ante sí una oportunidad de recuperación que puede compensar fácilmente el coste de la infraestructura subyacente.

El comercio agencial tiene un límite de confianza

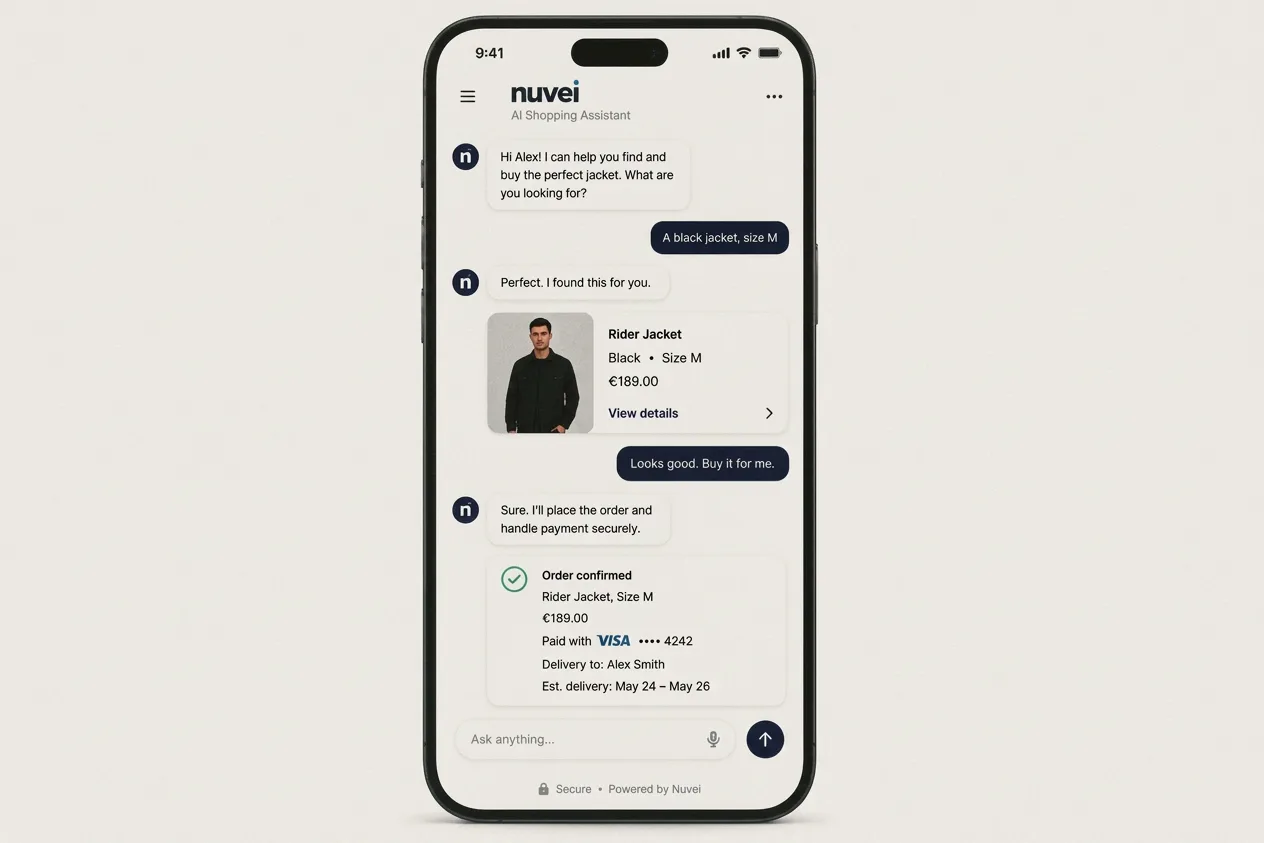

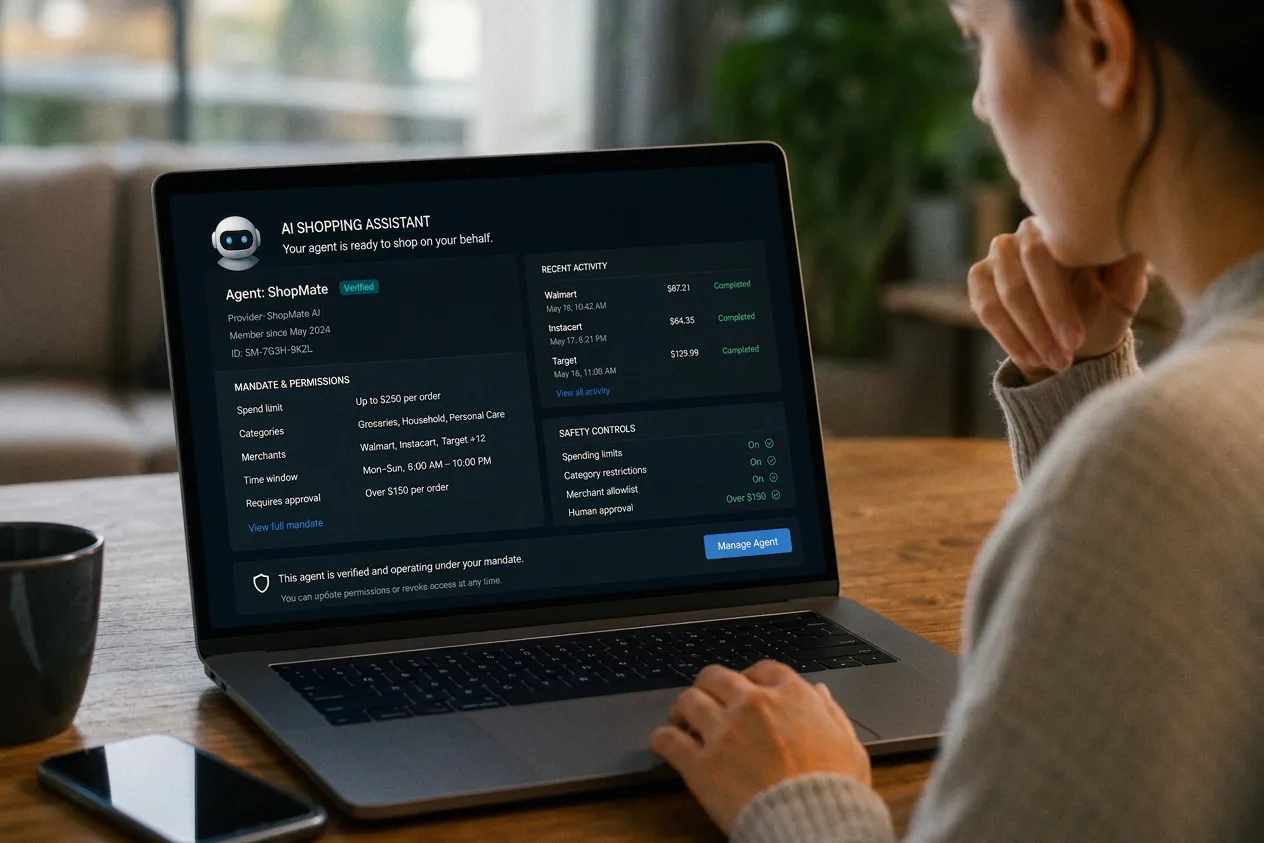

El debate sobre el comercio autónomo suele centrarse en lo que la IA puede hacer: buscar, decidir y realizar transacciones de forma autónoma. Los datos de «How America Pays» se centran en lo que los consumidores realmente están dispuestos a aceptar. El 40 % de los consumidores estadounidenses que ya se muestran abiertos a las compras asistidas por IA representan un valioso segmento de pioneros en la adopción de nuevas tecnologías. Es probable que esa cifra aumente.

Pero la confianza en las compras mediante IA crecerá de la misma forma que ha crecido la confianza en todas las innovaciones de pago: a través de una adopción visible, seguida de una infraestructura que haga que la experiencia resulte segura. Se trata de la misma lógica de confianza social que determina la adopción de los métodos de pago, aplicada a una decisión de mayor riesgo: ceder el control financiero a un sistema que el consumidor no puede observar directamente. Al igual que el comercio tuvo que recuperar la confianza cuando pasó del efectivo a las tarjetas, tendrá que volver a ganársela para la era de los agentes.

Es en las infraestructuras donde ocurre todo eso.

Como dice Hilla Peled, vicepresidenta sénior de IA y ciencia de datos en Nuvei: «El comercio agentivo rompe con las tres premisas en las que siempre se han basado los pagos: que un humano autoriza la transacción, que sabemos quién es y que los errores se pueden revertir. Quien consiga reconstruir esas tres premisas para los agentes se llevará la próxima década de los pagos».

Hoy en día, la confianza es una condición indispensable para el comercio mundial.

Los datos de «How America Pays » apuntan en la misma dirección en todos los ámbitos:

- Los consumidores quieren métodos de pago que les resulten familiares.

- Quieren tener el control sobre sus decisiones financieras.

- Y quieren que la experiencia de pago esté a la altura de la marca que les ha llamado la atención.

Cuando todo eso está en su sitio, se quedan. Cuando no, se van.

La forma en que empresas estos métodos determina el grado de seriedad con el que los consumidores los perciben. Pero los consumidores no adoptan nuevos métodos de pago solo porque las empresas los empresas . Los adoptan después de ver que gente que conocen los usa. La confianza suele extenderse socialmente antes de convertirse en un comportamiento generalizado, y eso crea una oportunidad comercial específica.

Cada pago cuenta una historia, y lo que nos revela este estudio es que el proceso de pago no es el final del recorrido de compra, sino más bien una continuación del mismo, un momento en el que la marca demuestra su valía. Los comerciantes que sabrán gestionar lo que viene después —incluidas las compras a gran escala impulsadas por la inteligencia artificial— son aquellos que lo entendieron a tiempo para construir su infraestructura en torno a ello.

Echa un vistazo a todos los datos de la encuesta aquí.