The four layers powering agentic commerce

What the infrastructure powering agentic payments will look like in practice.

Generative AI is still primarily a research and consideration layer, and the final click, at least for now, happens on a conventional site and belongs to a human, not a machine.

But while most public discussion still focuses on consumer-facing shopping assistants, the infrastructure transformation enabling agents to search, negotiate, and assist payments at scale is already operational - particularly in B2B flows, where consent and liability are clearer.

Early pilots show that eCommerce is quickly evolving into a multi‑agent ecosystem where public agents, merchant agents, payment service provider (PSP) agents, and card network agents negotiate and transact in real time. Each layer within this infrastructure has different roles and control points. And understanding them will determine merchants’ competitive advantage as agentic commerce scales.

Layer One - Consumer AI Platforms: The new gatekeepers of discovery

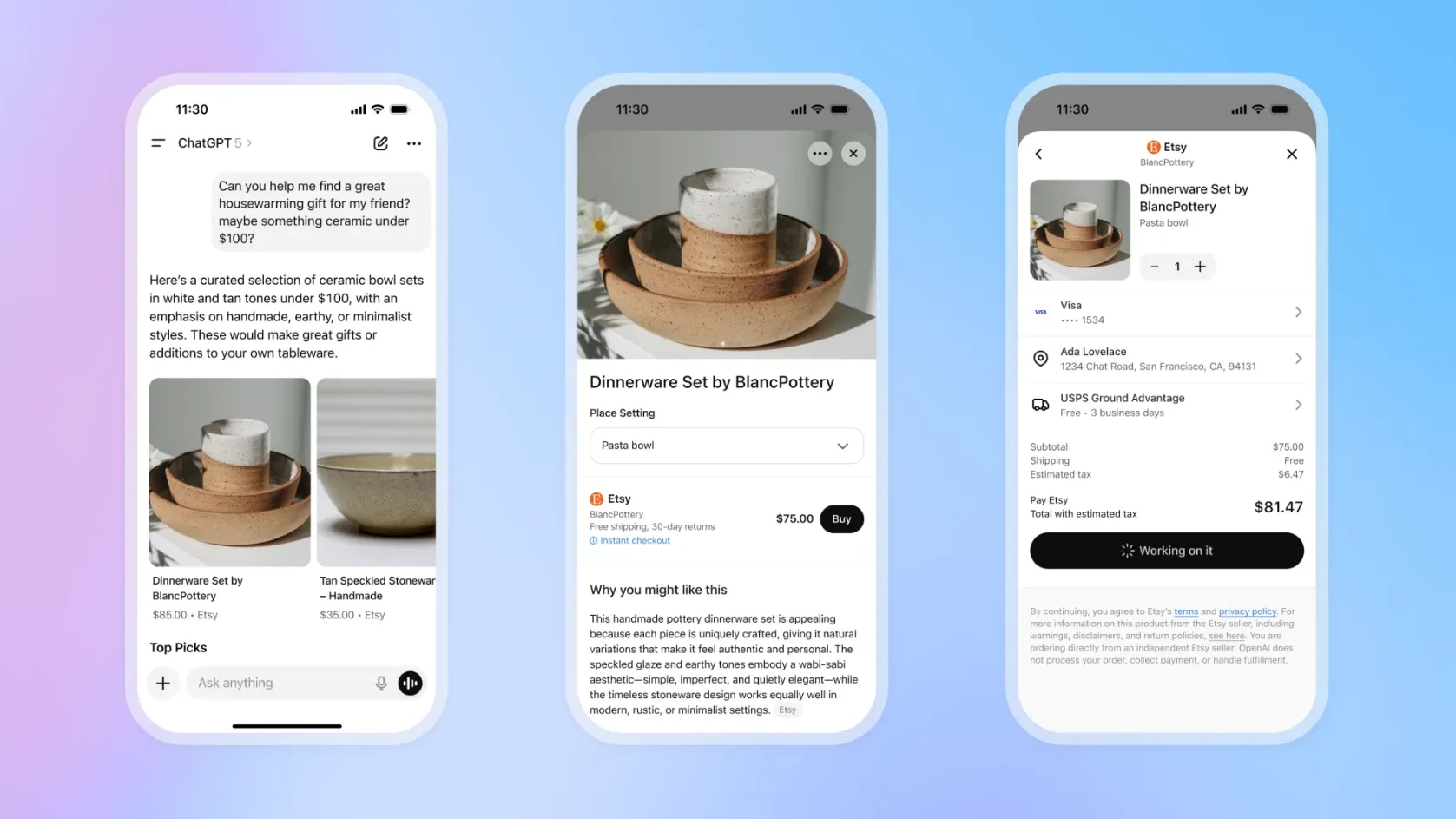

By late 2025, public AI platforms such as ChatGPT, Perplexity, and others had become major discovery channels that increasingly influence which merchants consumers visit.

On September 29, 2025, Mastercard's Agent Pay launched on ChatGPT, enabling U.S. cardholders to complete purchases directly within chat interfaces. Meanwhile, OpenAI partnered with Shopify to make over one million merchants discoverable and purchasable through ChatGPT's conversational flows.

Unlike humans, AI agents do not meaningfully scroll or interpret visual hierarchy - ChatGPT, Perplexity, Claude, Gemini, and others extract structured data from feeds, APIs, and schema.org markup.

Despite all the efforts of a merchant brand team, the homepage, banners, and UX flows carry little weight for an agent.

Instead, agents evaluate products as rows in a table with attributes, prices, availability, and policies they can parse and compare across multiple merchants.

Merchants with near-complete attribute coverage (95%+) in their product feed often report higher visibility in AI recommendations compared to sparse catalogs. On the other hand, agents routinely skip products with missing data like shipping windows, sizing, or return policies.

Best practices to maximize visibility for merchants in agentic commerce:

- Expose complete, structured product data via feeds and schema.org product markup so agents can reliably interpret the catalog.

- Align catalog structure to natural‑language queries (“waterproof hiking boots under £200 that deliver by Friday”), not just internal merchandising logic.

- Maintain real‑time inventory and pricing sync. Agents penalize outdated or inaccurate data and will quickly down‑rank merchants that routinely misrepresent stock or delivery promises.

- Provide agent‑friendly checkout APIs or adopt emerging agentic commerce standards to avoid brittle HTML scraping.

- Whitelist trusted agents while maintaining fraud defenses to distinguish beneficial automation from abusive bots.

As agentic commerce scales, merchants who optimize machine-readable data rather than (just) human persuasion will dominate agent-driven discovery. While those still building exclusively for pageviews could risk becoming invisible.

Layer Two - Merchant Agents: From visibility to owning outcomes

Even if you've done all the optimization for public agents, you might have visibility, but you still don't have control over the brand experience, transaction outcome, or how your message is transmitted to consumers. Recent industry surveys indicate most large retailers expect agentic payments to become mainstream within three years, yet many have not yet defined how their systems will handle agent-initiated purchases, post-purchase modifications, or refunds when operating at scale.

This is where a bespoke merchant agent comes into play.

When a public agent arrives with a request such as “a £120 running shoe shipping by Tuesday,” a merchant agent interprets the intent, maps it to the merchant’s catalog and logistics, and assembles the best offer that merchant can make. It can manage real‑time inventory constraints, choose shipping and fulfilment options that meet the deadline, and maintain brand voice in how products and trade‑offs are presented. Rather than leaving it to a public agent to scrape pages and guess, merchant agents become active negotiating counterparts that can adjust bundles, apply promotions, and propose alternatives when an exact match does not exist.

Over time, merchant agents are likely to become the default interface to PSPs and schemes. They will surface real‑time inventory, pricing, and risk signals that other layers of the infrastructure can optimize against. In that model, the public or broker agent orchestrates across multiple merchants, while each merchant agent focuses on maximizing conversion, margin, and customer experience for its own business.

In agentic commerce, the future belongs to merchants who have built agents to actively shape transactions and own outcomes, not merely waiting to be discovered.

Layer Three - Payment Agents: The operational intelligence center

Agents within PSPs and global payment platforms like Nuvei increasingly handle the operational intelligence that turns intent into money movement at scale. They own fraud detection, routing optimization, authorization performance, dispute management, reconciliation, treasury decisions, and compliance enforcement across thousands of merchants and millions of transactions. As these control points converge in agentic commerce, the intelligence payment platforms will generate can compound across the entire value chain.

A payment agent can operate within one of the following control points:

- Checkout and funding. Determining whether a transaction should be approved, which funding source to use, and which fraud signals to apply in real time. Intelligence here means learning new patterns of agent behavior and adapting as agents evolve.

- Authorization and routing. Deciding whether to send a transaction through 3D Secure, which acquirer or route to choose based on live performance, and whether to bid dynamically on fees and routing paths. Recent case studies show that AI‑driven routing and risk optimization can reduce fraud losses by more than half and lift approval rates enough to deliver high‑single‑digit revenue uplifts for some merchants, especially in cross‑border and higher‑risk segments.

- Post‑payment controls. Optimizing chargeback evidence, fund release timing, and liquidity management, with decisions that compound across thousands of transactions per day.

PSPs and payment platforms with globally distributed data, multi‑acquirer global setups, and embedded AI decisioning will be better positioned to train agent‑aware models across geographies and use cases.

The intelligence received from such PSPs can become a shared asset for merchants who want to benefit from agentic commerce without building every capability themselves and the entire infrastructure powering agentic commerce.

Layer Four - Scheme Agents: Encoding trust and standards

Card networks are evolving beyond passive payment rails into intelligent orchestration layers that differentiate agents from human transactions and apply context‑specific security models.

For example, in October 2025, Visa unveiled its Trusted Agent Protocol (TAP) - developed with Cloudflare - to provide cryptographic verification for AI agents during browsing and checkout. With it, merchants and PSPs can distinguish trusted agents from malicious automation with minimal changes to their infrastructure.

Meanwhile, Mastercard is working with partners including Microsoft, IBM, and Google to scale agentic commerce globally, and has announced plans to expand Agent Pay across Latin America.

Scheme agents are beginning to detect and classify “agent-present” transactions via:

- Trusted Agent Protocol (Visa): Cryptographic signatures verify agent identity during browsing

- Agent Pay (Mastercard): Special credentials prove "I'm ChatGPT acting for Alex B"

Scheme agents spot agent traffic through cloud IPs, automation fingerprints, and protocol flags. These distinguish legitimate agents from humans and malicious bots, then apply agent-specific rules such as lower friction for trusted agents, tighter scrutiny for unknown ones. They also coordinate authentication by preserving agent identity signals through the PSP → issuer → settlement flow.

What remains undeveloped is broad, interoperable adoption of these standards, as well as clear liability rules that define what happens when an authorized agent makes a harmful decision on behalf of a consumer – or a business.

As agentic commerce scales, scheme agents will increasingly be responsible for coordinating authentication, applying context‑aware fraud models, and enforcing emerging “agent‑present” categories that sit alongside today’s card‑present and card‑not‑present distinctions.

At the same time, schemes are exploring how card network protocols (such as TAP and Agent Pay) could extend toward APM interoperability.

Is your payment infrastructure ready for agentic commerce?

Industry surveys suggest that close to 60% of banks and large corporations expect agentic payments to be mainstream within the next three years, with early adoption clustering around recurring billing and B2B purchasing flows.

It is likely only a matter of time before these patterns extends more broadly into B2C, particularly for repeat and low-risk purchases. eCommerce is evolving into a multi-agent ecosystem, where human intent is increasingly expressed indirectly rather than through clicks.

For merchants, the question is less whether agents are coming and more whether their infrastructure will be ready when agents become a primary interface for purchase.

[1] https://www.trade.gov/country-commercial-guides/japan-ecommerce-0 [2] https://www.nuvei.com/jp/posts/nuvei-launches-in-japan. [3] https://www.researchandmarkets.com/reports/5987254/japan-online-retail-forecast-28

Asaf Ben Gal is Director of AI & Analytics at Nuvei, leading the company’s AI strategy and applied machine learning initiatives to turn advanced technologies into measurable business impact.

Ready to grow everywhere?

Get started with Nuvei – the growth infrastructure for every payment, everywhere. One intelligent system, built to scale.