How well do you know your agent?

Why delegated trust will define the next era of payments.

For years, the payments industry rested on a simple comfort: a human thumbprint on every purchase. A tap of a card. A biometric scan. A 2FA prompt. That pattern held through contactless, digital wallets, and one-click checkout. Agentic commerce breaks it.

The human is no longer at the glass, authorizing in the moment. Authority is delegated in advance to an AI agent that can discover, decide, and attempt to transact on a consumer's behalf.

The question is no longer whether a payment can be processed. It is who, or what, is authorizing it, what that actor is allowed to do, and who is liable when something goes wrong.

That gap has a name: Know Your Agent, or KYA. And it points to a larger shift. The control point of commerce is moving away from the checkout page and toward the layer that can verify an agent, enforce what it is allowed to do, and route its transaction through the right rails. Whoever operates that layer operates agentic commerce.

Agentic commerce is already here

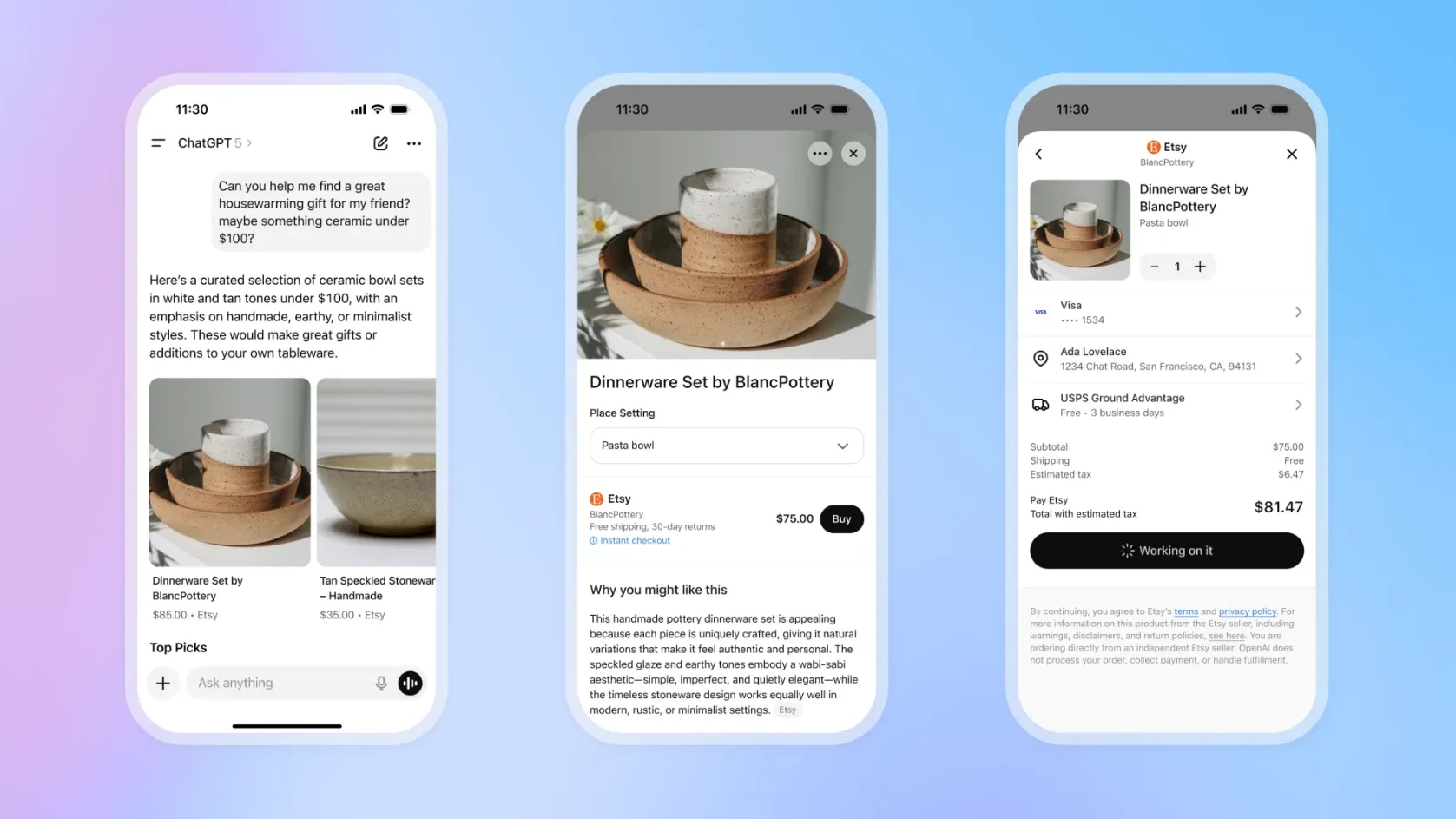

In 2026, agentic commerce is no longer a thought experiment confined to conference panels. AI sits inside the shopping journeys of hundreds of millions of consumers, who use general-purpose models and retailer assistants to search, compare, and narrow purchase decisions. In some cases they already let AI help at checkout.

Consumers have invited AI into the decision layer and are hesitating at the transaction layer. Nuvei's How Agents Pay research shows that 58% of consumers find AI useful for researching products and comparing prices, and 39% say they are using AI while shopping more often than they were only three months ago. Yet only 27% would feel comfortable storing payment credentials on an AI platform, and 28% would feel comfortable letting it complete a purchase automatically.

The buyer of record at checkout is now, more often, an agent acting on behalf of a person, and adoption is moving faster than the infrastructure built to govern it. McKinsey estimates that agentic commerce could drive trillions of dollars in global retail spend by 2030, which turns today's gaps in trust, liability, and standards into an urgent problem rather than a theoretical one.

Knowing your customer is no longer enough

Traditional payment systems were built for a human buyer. A person sees the transaction, recognizes it, authorizes it, and can dispute it later. Fraud controls, dispute rules, and liability frameworks were all designed around that pattern. When the buyer is an AI agent, the pattern breaks.

The control point in commerce is shifting. It is no longer the checkout page. It is the layer that can interpret an agent's intent, verify its mandate, and route the transaction through the right rails with the right controls.

That layer has to answer a different set of questions.

- Is this agent what it claims to be?

- On whose behalf is it acting?

- What has the consumer authorized, in amounts, categories, time windows, and named merchants?

- And what evidence survives a dispute when no human ever pressed pay?

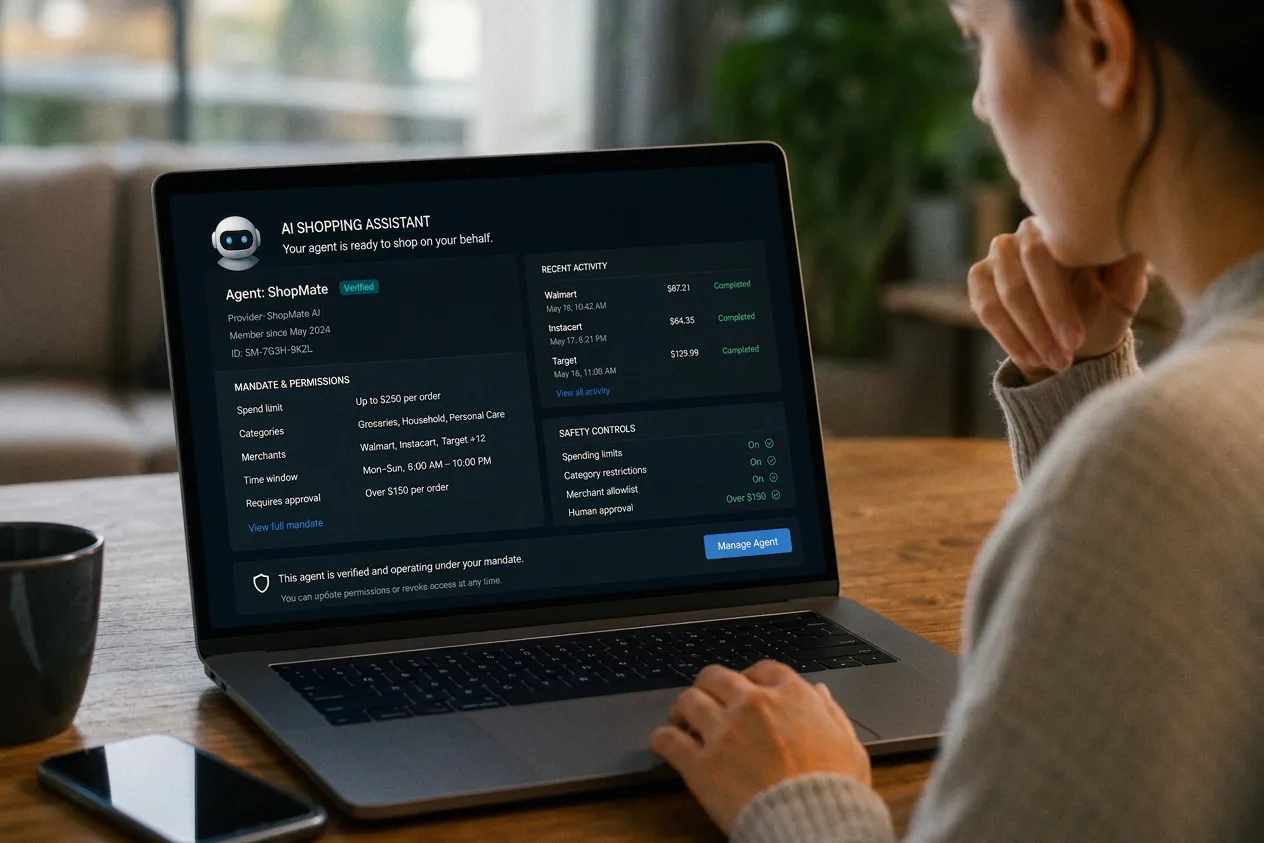

Know Your Customer has been foundational in financial services for decades. It verifies the human behind the account. In an agentic world that work remains necessary, and it is no longer sufficient. The system now needs a way to verify the agent itself, its identity, its mandate, and its behavior, before it touches the payment flow. That is what KYA is for. It extends the compliance logic of KYC from humans to the non-human actors entering commerce, and it establishes an agent's identity, authority, and behavioral boundaries before the agent can initiate or complete a transaction.

Early work is underway. New protocols are starting to carry trust signals about agents, including their provenance and capabilities. The market is still defining what production-grade agent identity, mandate handling, and reputation scoring should look like, and how that information should move between AI platforms, merchants, payment providers, and issuers. Until KYA is built into the infrastructure, agentic commerce stays promising and incomplete.

When standards multiply

The identity problem would be hard enough on its own. The protocol landscape is multiplying at the same time. Several agent frameworks are emerging to define how AI agents talk to merchants, payment providers, and one another in order to discover, negotiate, and complete transactions. Each speaks a slightly different dialect. From a merchant or PSP's point of view, the picture is familiar and uncomfortable: no one wants to rebuild a payment flow five times to keep pace with the latest protocol.

What the market lacks is an execution layer that sits between agents and payment rails. One that abstracts the protocol differences, enforces mandates and limits, and translates an agent's intent into trusted, local transactions. That layer cannot be a cosmetic patch or a single line on a roadmap. It has to be operational, certified, and connected to the places where commerce already happens: gateways, acquirers, local payment methods, and issuer rails.

This is where the control point sits: at the execution layer that brings agent identity, mandate enforcement, and local routing into one place. It belongs at the PSP, gateway, and acquirer level, because that is where trust signals and money movement already meet, below the model and beneath the checkout page.

Local still wins, even for agents

The medium is new. Customer preference is not. A consumer in São Paulo who asks an AI assistant to reorder groceries still expects to pay with Pix. A voice-driven booking in Mumbai still needs UPI. A Perplexity-assisted purchase in the United States still has to work with the method the buyer prefers. Agentic commerce is global by design. Commerce stays stubbornly local at the point of payment.

If the acquiring path is wrong, the preferred method is missing, or local risk rules are ignored, the transaction fails as fast as it would for a human shopper. In agentic commerce that failure costs more, because the promise of the model is speed and delegation. When the agent cannot complete the purchase on the right rail, it does not wait. It moves to the merchant that can.

This is why trust and local execution belong together. They are the same problem seen from two sides. Trust without execution fails, because a verified agent that cannot pay on the right rail still loses the sale. Execution without trust is dangerous, because a transaction that completes without a verified mandate is a liability waiting to surface. Agentic commerce requires both to be solved in the same place, by the same layer.

From acceptance to trust

In the last era of payments, the defining challenge was acceptance: receiving, routing, and settling payments from any card or method wherever a merchant operates. In the agentic era, the defining challenge is trust. Who is liable if the agent buys the wrong item? What happens when it duplicates a transaction? How do you enforce per-user limits when one agent is booking travel for an entire team? What does friendly fraud look like when the consumer never pressed the button?

Few providers have a complete answer today. Connecting to an agent is the easy part. The advantage belongs to the providers that can verify trust, enforce intent, and carry the transaction across the right local rails, all in the same place. A provider like Nuvei, already running local acquiring in more than 50 countries, with connectivity across more than 200 and more than 720 payment methods, starts from the rails the agent will need on the other side of the decision . Pair that reach with agent verification and mandate enforcement, and the question at the center of commerce changes. It moves from can we accept this payment to can we trust this agent, on this mandate, on these rails.

The first era of digital commerce was about acceptance. The next era is about delegated trust. The infrastructure that wins will not just move money. It will decide when it should move, and on whose authority.