Canada’s ecommerce market is on track to grow from $63.2 billion in 2024 to nearly $92 billion by 2030, with 2026 well within that expansion curve. What deserves closer attention is how much of that growth Canadian businesses are actually converting.

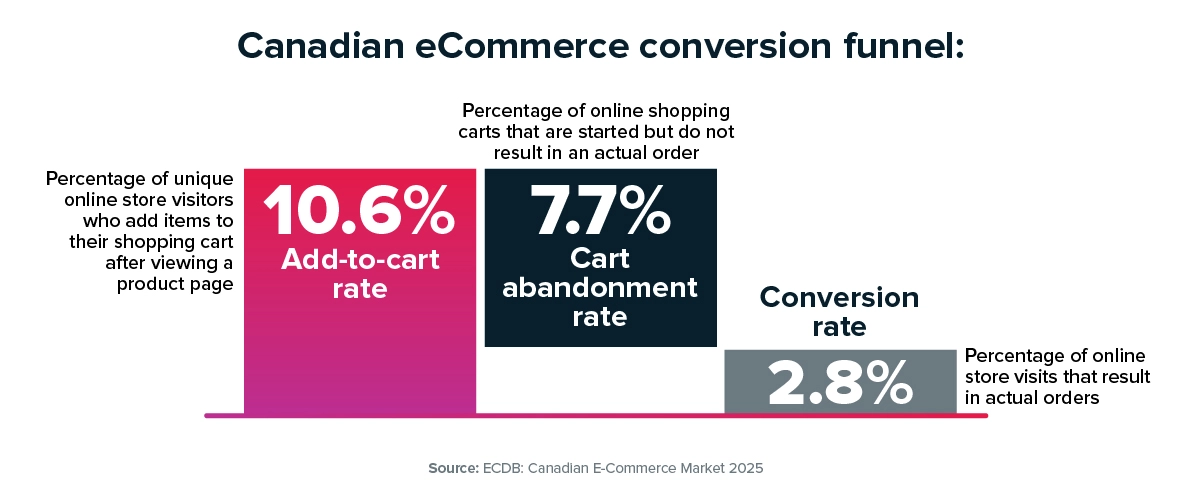

Average ecommerce conversion in Canada sits at 2.8%, with an add-to-cart rate of 10.6%. At those levels, performance gains are incremental rather than dramatic. When a transaction is declined at authorization, the loss occurs after acquisition spend has been committed, product selection confirmed, and checkout completed. In a market approaching $70 billion annually, even small improvements in approval performance translate into significant revenue differences.

Understanding where those improvements can be realized starts with how Canadians pay and how those payments are evaluated.

Canada’s card-dominant eCommerce market and the role of issuer decisioning

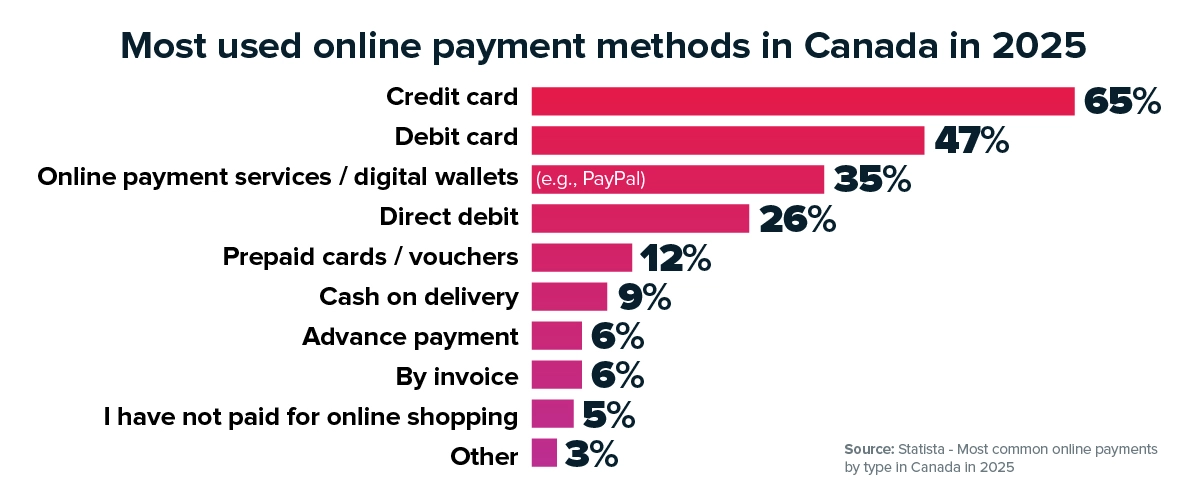

Canada remains structurally card-led. In 2025, 65% of online shoppers used credit cards, 47% used debit cards, and 35% used online payment services or digital wallets. Credit card usage has remained stable across ecommerce and point of sale, and even cost-of-living pressure has strengthened its role: 53% of Canadians reported increasing their use of credit cards in response to rising living costs.

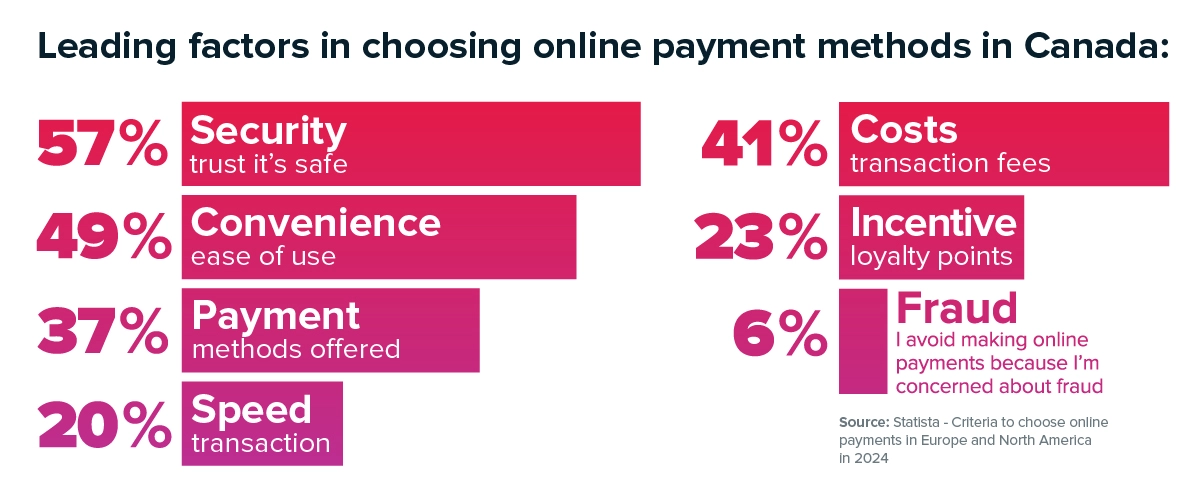

Payment preferences reflect similar dynamics. When Canadians are asked what determines their choice of online payment method, security and trust rank highest at 57%, followed by convenience at 49% and transaction fees at 41%. Fraud remains a visible concern in the market, influencing how both consumers and issuers approach transactions.

In a card-dominant environment, issuer decisioning plays a decisive role in eCommerce performance. Issuers evaluate geography, transaction consistency, data completeness, authentication context, and historical behavior before approving a payment. When transaction signals align with expected patterns, approvals tend to be smoother. When they do not, additional scrutiny follows. The difference often lies in how the transaction is structured and presented upstream.

Domestic eCommerce in Canada: why local payment optimization matters

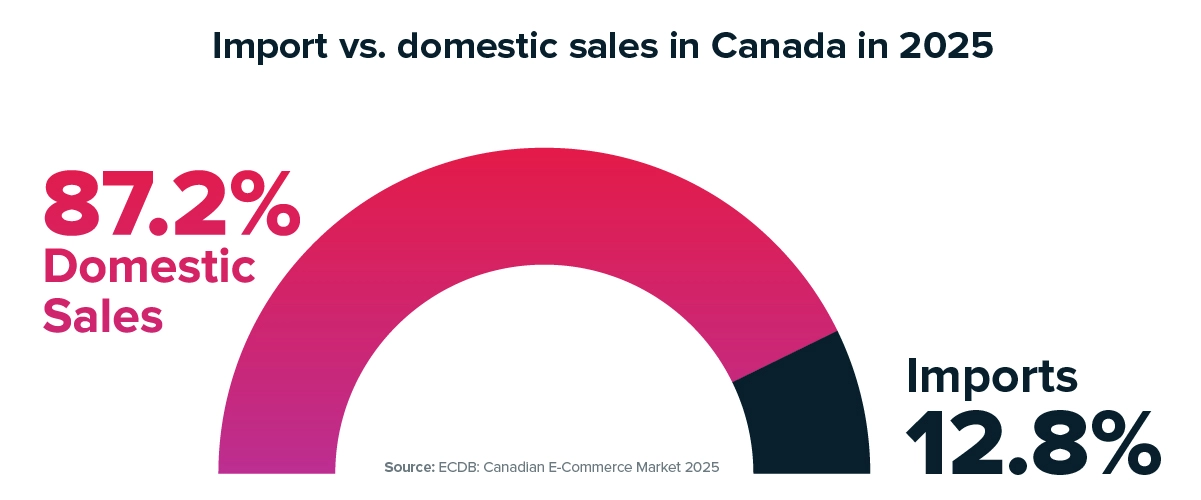

This becomes even more relevant when considering that 87.2% of Canadian ecommerce revenue is domestic, with imports accounting for just 12.8%. Most revenue is generated within Canada itself, and most performance gains are therefore found in optimizing domestic flows. At the same time, future real-time rails remain in phased development, meaning card and debit infrastructure will continue to underpin the majority of online revenue in the near term. For now, performance lives primarily within the existing card ecosystem, and that ecosystem rewards precision.

Direct local acquiring in Canada and what it changes for merchants

Local acquiring shapes how much visibility and control a merchant has over payment performance. Our analysis of global payment acceptance data shows that processing transactions through local acquiring can improve acceptance rates by up to 16%, largely because transactions are presented to issuers with more consistent geographic and risk signals.

When transactions pass through intermediaries, oversight becomes fragmented. Data is available, but not always at the level needed to understand why approvals fluctuate or processing costs increase. Routing changes require coordination across multiple parties, and identifying emerging patterns can take time. Interchange components appear in reporting, yet isolating their drivers is not always straightforward.

Processing domestically through a direct acquiring model reduces that distance. The path between merchant and issuer becomes shorter, transaction-level data becomes clearer, and routing logic can be adjusted with more precision. Instead of relying on aggregated reporting after the fact, merchants can manage performance closer to where authorization decisions are made.

Fewer external processing layers also reduce reconciliation friction and create tighter alignment between acceptance, optimization, risk management, and payouts. As businesses expand across channels or scale beyond domestic borders, having those functions connected within a unified framework supports steadier execution.

Debit and payment cost optimization in Canadian ecommerce

Debit strategy adds another layer to that equation. While credit cards dominate usage, 47% of Canadian online shoppers report using debit cards, and Interac remains one of the country’s most trusted payment brands, underpinning a substantial share of Canadian transactions.

Blended processing cost is influenced by card mix as credit and debit transactions are priced differently at the network level. Routing capabilities that allow eligible transactions to flow through domestic debit rails can shift effective cost per transaction without altering the customer experience. When acquiring configuration does not support that flexibility, merchants default to less optimized pathways.

Fraud prevention, issuer scrutiny, and authorization rates in Canada

Fraud pressure further complicates the landscape. Fraud prevention remains central to the evolution of Canada’s payment infrastructure, and increased fraud exposure typically leads issuers to tighten thresholds. Stricter thresholds increase scrutiny, particularly when transaction data lacks clarity or consistency. Authorization performance therefore depends on how effectively fraud controls are balanced with transaction quality and routing precision.

Consolidated data flows and adaptive routing improve that balance. Fragmented acquiring environments slow adjustments and reduce visibility into issuer behavior. The ability to respond quickly becomes a competitive advantage.

Capturing the next $30B in Canadian ecommerce through payment precision

Canadian ecommerce is projected to expand by nearly $30 billion between now and 2030. That growth will not be captured evenly. Credit cards will continue to dominate online spending, debit through Interac will remain significant, and real-time payments will mature gradually. Security expectations will remain high, and issuer scrutiny will continue to shape approval outcomes.

In this environment, acquiring decisions increasingly influence revenue retention and cost optimization. Nuvei’s direct acquiring capability in Canada forms part of a broader infrastructure model that combines local processing, intelligent routing, and unified reporting across markets. For merchants, this means stronger approval predictability, clearer cost visibility, and a more stable foundation for scaling domestically and internationally.

Want to explore how local acquiring could improve payment performance for your business? Connect with our team to discuss what we’re seeing across Canadian ecommerce and how it could inform your payments strategy.